Moving insurance is defined as a liability coverage that protects your belongings during a relocation, with protection levels, costs, and claim processes varying significantly depending on the option you select. Most people assume their mover carries full responsibility for any damage. The reality is quite different. Federal regulations in the US, governed by 49 CFR Part 375 and overseen by the Federal Motor Carrier Safety Administration (FMCSA), require interstate movers to offer two distinct valuation options. Understanding moving insurance explained properly means knowing the difference between those mandated options and true third-party insurance policies, which are regulated separately by state insurance commissioners.

This guide walks you through every option, what it costs, and how to choose the right cover for your move.

What moving insurance options are legally required?

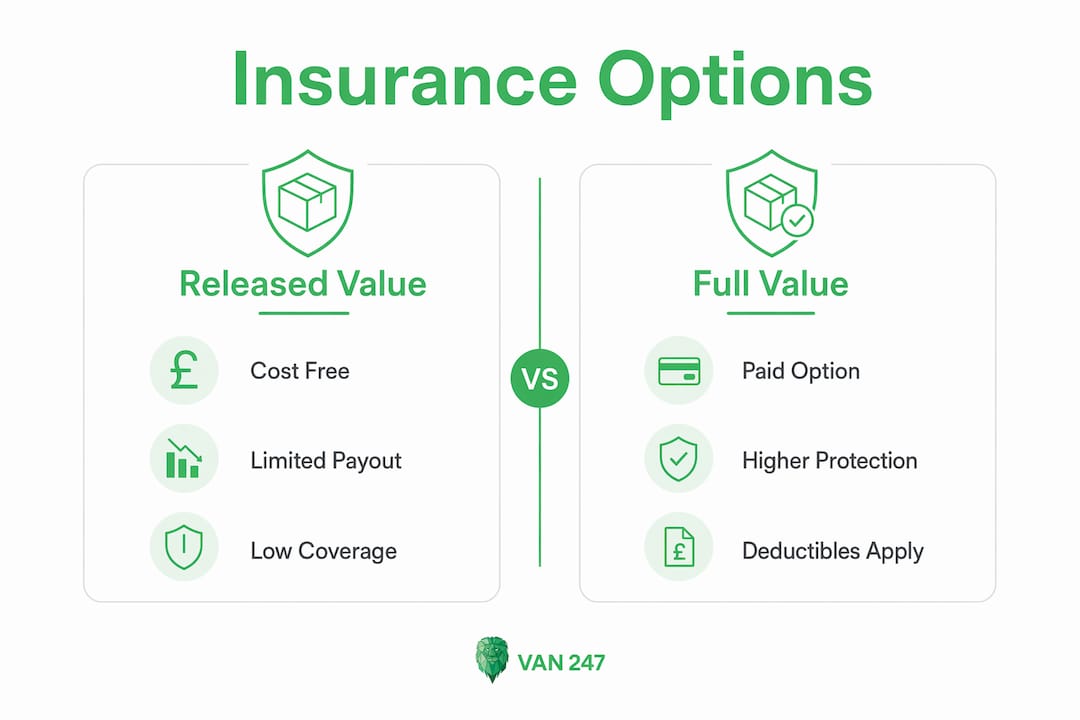

Interstate movers must offer two valuation options by law: Released Value Protection and Full Value Protection. These are not insurance policies in the traditional sense. They are contractual liability agreements between you and your mover, which is a distinction that matters enormously when a claim goes wrong.

Released Value Protection

Released Value Protection is the default option and costs you nothing. The catch is significant. Coverage pays only £0.60 per pound per item, regardless of actual value. A 10lb television worth £1,500 would receive a payout of just £6. That figure illustrates exactly why Released Value Protection protects movers far more than it protects you. Accepting it without understanding the implications is effectively self-insuring your entire shipment for pennies per pound.

Full Value Protection

Full Value Protection is the paid alternative and gives you considerably more recourse. Under this option, your mover must repair a damaged item, replace it with a comparable one, or pay you its current market value. Full Value Protection typically costs between 0.5% and 1.5% of your declared shipment value. On a £50,000 shipment, that translates to roughly £250 to £750.

There are important limitations to understand. Deductibles commonly range from £250 to £500, and cash payouts may reflect depreciated rather than replacement value. Items packed by you rather than the mover are typically excluded unless you declare them separately. The mover also retains discretion over whether to repair, replace, or pay cash, which can lead to disputes.

Pro Tip: Always request Full Value Protection in writing before moving day. Verbal agreements carry no weight if a claim arises.

| Coverage type | Cost | Payout basis | Owner-packed boxes |

|---|---|---|---|

| Released Value Protection | Free | £0.60 per pound per item | Included but minimal payout |

| Full Value Protection | 0.5%–1.5% of declared value | Repair, replace, or cash value | Usually excluded |

| Third-party insurance | 1%–5% of declared value | All-risk or named-peril basis | Often included |

How does third-party moving insurance differ from mover-provided cover?

Third-party moving insurance is a genuine insurance product, sold by a licensed insurer and regulated by state insurance commissioners. That regulatory difference changes everything about how your claim is handled. When you buy a third-party policy, you deal with an insurer, not the moving company, which removes a significant conflict of interest from the process.

The practical benefits over mover-provided valuation cover are substantial:

- All-risk or named-peril cover: Third-party policies often cover a broader range of causes, including accidents during loading, transit, and unloading.

- Owner-packed boxes: Many third-party policies cover boxes you packed yourself, which Full Value Protection typically excludes.

- Subrogation: The insurer pays you first, then pursues the mover for reimbursement. You avoid a direct dispute with the company handling your belongings.

- Independent claims process: Your claim is assessed by an independent adjuster, not the mover’s own team.

- Regulatory protection: State insurance commissioners oversee the insurer’s conduct, giving you a formal escalation route if a claim is mishandled.

The cost is higher. Third-party cover costs between 1% and 5% of declared value, meaning a £50,000 shipment could cost up to £2,500 to insure fully. Whether that premium is worth paying depends on what you are moving and how much you can afford to lose.

Pro Tip: Compare exclusion lists, not just premiums. Insurance experts recommend reviewing exclusions carefully, because a cheaper policy with broad exclusions can leave you worse off than a pricier one with genuine all-risk cover.

One more thing worth knowing: your home contents or renters insurance may offer some cover during a move. However, many home insurance policies exclude damage caused by movers or accidents in transit, and high deductibles can make claims uneconomical. Check your existing policy before assuming you are covered. You can also read more about valuation versus insurance cover to clarify which type of protection suits your situation.

What to consider when choosing moving insurance for your relocation

Choosing the right cover is not complicated once you know what to look at. Work through these four considerations before signing anything.

- Calculate your shipment value accurately. Add up the replacement cost of every item being moved. Under-declaring your shipment value results in proportional claim payouts. Declared value must be accurate, because over-declaring inflates your premium without adding any benefit.

- Identify high-value items separately. Jewellery, antiques, artwork, and collectibles often fall outside standard mover coverage. Declaration thresholds are often set at £100 per pound, and items above that threshold require additional declarations and sometimes separate specialist insurance. List these items individually on your inventory before moving day.

- Consider who is packing your boxes. If you pack your own boxes, Full Value Protection almost certainly will not cover them. Either pay for professional packing or choose a third-party policy that explicitly covers owner-packed items. Read more about how packaging affects your cover before you decide.

- Weigh deductibles against likely claim amounts. A £500 deductible on Full Value Protection means small claims cost you nothing to pursue. If your most valuable item is worth £600, the deductible makes a claim barely worthwhile. Third-party policies often offer lower deductibles in exchange for a higher premium, which can be the better deal for high-value shipments.

For stress-free planning that goes beyond insurance, moving organisation tips can help you prepare your inventory and documentation well in advance.

How to protect your belongings and file a claim if damage occurs

Good documentation is the single most important thing you can do before, during, and after your move. A well-documented claim is far more likely to succeed than one filed from memory weeks later.

- Photograph everything before packing. Take clear photos of all furniture, electronics, and fragile items. Capture existing scratches, dents, or wear. These images establish pre-move condition and are your strongest evidence if damage is disputed.

- Use a detailed inventory sheet. List every item with its estimated replacement value. Your mover should provide an inventory form, but create your own as a backup. Note the condition of each item at the point of collection.

- Inspect your delivery immediately. Do not sign the delivery receipt until you have checked every item. Note any damage on the receipt in writing before the driver leaves. Signing without noting damage can weaken your claim significantly.

- File your written claim promptly. Federal regulations require claims to be filed within 9 months of delivery for interstate moves. Once filed, your mover has 30 days to acknowledge the claim and 120 days to settle or deny it. Missing the 9-month window forfeits your right to compensation entirely.

- Escalate if necessary. If your claim is denied or undervalued, you have options. For mover-provided valuation, request arbitration through the mover’s dispute resolution programme. For third-party insurance, escalate to your state insurance commissioner. Small claims court is also an option for lower-value disputes.

Pro Tip: Keep copies of all correspondence with your mover and insurer. A clear paper trail is your best asset if a dispute reaches arbitration or court. For broader guidance on keeping your move safe and organised, the safe moving guide for 2026 covers practical steps from packing to delivery.

Key takeaways

Moving insurance and valuation coverage are not the same thing, and choosing the wrong option can leave you significantly undercompensated for damaged or lost belongings.

| Point | Details |

|---|---|

| Released Value is inadequate | Default cover pays only £0.60 per pound, making it unsuitable for valuable items. |

| Full Value Protection has limits | Deductibles of £250–£500 apply, and owner-packed boxes are usually excluded. |

| Third-party insurance offers more | State-regulated policies often cover owner-packed items and use subrogation to handle disputes. |

| Declare value accurately | Under-declaring reduces your payout; over-declaring raises your premium without benefit. |

| File claims within 9 months | Federal law sets a 9-month filing window for interstate moves. Missing it forfeits your claim. |

Why I think most people get moving insurance badly wrong

People confuse valuation coverage with insurance constantly, and it costs them. I have spoken with movers who genuinely believed their belongings were “fully insured” because they ticked the Full Value Protection box, only to discover their owner-packed boxes were excluded and their cash payout was depreciated. That gap between expectation and reality is where most of the frustration in moving claims originates.

The uncomfortable truth is that Released Value Protection exists primarily to limit mover liability, not to protect you. Accepting it without reading the terms is one of the most common and costly mistakes people make during a move. If your shipment contains anything you could not comfortably replace out of pocket, Released Value is not a real safety net.

My honest recommendation is to treat moving insurance the same way you treat travel insurance: buy it before you need it, read the exclusions carefully, and do not assume the cheapest option covers what you think it covers. Third-party policies cost more, but the subrogation benefit alone, where the insurer handles the dispute with your mover so you do not have to, is worth serious consideration for any move involving high-value items.

The other thing I would stress is documentation. I have seen claims fail not because the damage was disputed, but because there was no photographic evidence of pre-move condition. Spend 30 minutes photographing your belongings before packing. It is the cheapest form of protection available to you.

— Claudiu

Moving with Van-247delivery: insured and protected from start to finish

Planning a move and want the reassurance of knowing your belongings are in safe hands?

Van-247delivery has provided professional, insured moving services across the UK for over 15 years. Every house removal is handled by experienced teams trained to protect your belongings throughout loading, transit, and delivery. Insurance cover is built into the service, so you are not left piecing together protection from separate providers. Whether you are moving a studio flat or a family home, Van-247delivery offers flexible booking, instant quotes, and the kind of careful handling that makes a real difference on moving day. Get in touch to find out what cover is included with your move.

FAQ

What is moving insurance and is it the same as valuation cover?

Moving insurance is a genuine insurance product sold by a licensed insurer, while valuation coverage is a contractual liability agreement offered by your mover. They differ in regulatory oversight, claims process, and the level of protection provided.

How much does Full Value Protection cost?

Full Value Protection typically costs between 0.5% and 1.5% of your declared shipment value. On a £50,000 shipment, that equates to roughly £250 to £750.

Are owner-packed boxes covered by moving insurance?

Mover-provided Full Value Protection usually excludes owner-packed boxes. Many third-party insurance policies do cover them, so check the policy wording carefully before you pack.

How long do I have to file a moving damage claim?

Federal regulations require you to file a written claim within 9 months of delivery for interstate moves. Your mover then has 30 days to acknowledge the claim and 120 days to settle or deny it.

Do I need separate insurance for high-value items?

Yes. Jewellery, antiques, and artwork often exceed standard declaration thresholds and require separate declarations or specialist cover. Standard mover coverage caps payouts at a set rate per pound, which is rarely sufficient for high-value pieces.